According to 2020 data, the average cost of property damage for vehicular accidents is around $4,700 per vehicle and could go even much higher. If you’re unlucky enough to be in a car accident you did not cause, who will foot the bill for the pricey repairs to your vehicle?

Don’t fret because there are legal options you can consider. One is to file a mini-tort claim or a limited property damage liability that allows the at-fault driver to pay for your car’s repair costs. While it may seem simple, proving a mini-tort can also be complicated, and you must be able to meet specific requirements to qualify.

To improve your chances of a successful mini-tort claim, talk to a Michigan car accident lawyer and read about the basics of this law below.

What Is a Mini-Tort Claim?

A mini-tort claim allows you to seek limited compensation for property damage from the at-fault driver if you are involved in a vehicle accident you did not cause. It is vital to understand that a mini-tort claim is intended to seek damages for vehicle repair costs (not injuries). You will be compensated through a separate claim if you sustain physical or emotional harm due to the accident.

Several U.S. states, including Michigan, have adopted a no-fault auto insurance system. Under the no-fault insurance, your insurance company compensates you for your own medical expenses and certain economic losses, regardless of who caused the accident. However, no-fault insurance does not cover repairs to your car if it’s damaged in an accident, except in specific situations like when your parked car is hit by another vehicle.

A mini-tort claim comes into play when you’re involved in a minor car accident, and the driver who caused the accident is identified. You can file a mini-tort claim against the at-fault driver to recover the cost of repairs that exceed your coverage. However, you can only recover the amount up to the limit set by the state.

How Does a Michigan Mini-Tort Law Work

Under Michigan auto insurance law, you can sue another driver and file a mini-tort claim. If the damage to your vehicle exceeds your insurance coverage and the other driver is found to be more than 50% at fault, a mini-tort claim is a good way to cover your deductibles.

In a Michigan mini-tort claim, the amount of compensation will be weighed depending on the drivers’ “faults.” The at-fault driver found to be more than 50% at fault will pay for the majority of the damage, while you will be responsible for the rest of the cost. If you have collision coverage, the mini-tort compensation will mostly be enough to cover your deductibles.

However, if you don’t have collision coverage and the mini-tort is your only source to pay for the damage, you might have to face the costs if the damage is extensive. Ultimately, the mini-tort claim is not meant to pay for the entire damage cost but only a small compensation due to negligence.

When to File a Mini-Tort Claim

In Michigan, proving who caused the accident is crucial in filing a mini-tort claim. There are also other factors you need to show and prove. Here are some of them:

-

- The vehicle is damaged.

- Show that the other driver was more than 50% at fault for the accident.

- Michigan’s no-fault insurance must cover your vehicle.

- The damage to your vehicle exceeds or isn’t part of your coverage.

Mini-Tort Claim Exclusions

Several conditions can disqualify your mini-tort claim. Here are some of them:

-

- If you fail to identify the at-fault driver.

- If it’s proven that you were more than 50% at fault or responsible for the accident.

- It cannot cover medical costs, loss of wages, and other non-vehicular damages.

- Under Michigan’s No-Fault law, motorcycles are not motor vehicles and cannot be eligible for a mini-tort claim.

- It will not cover more than $3,000 in damages.

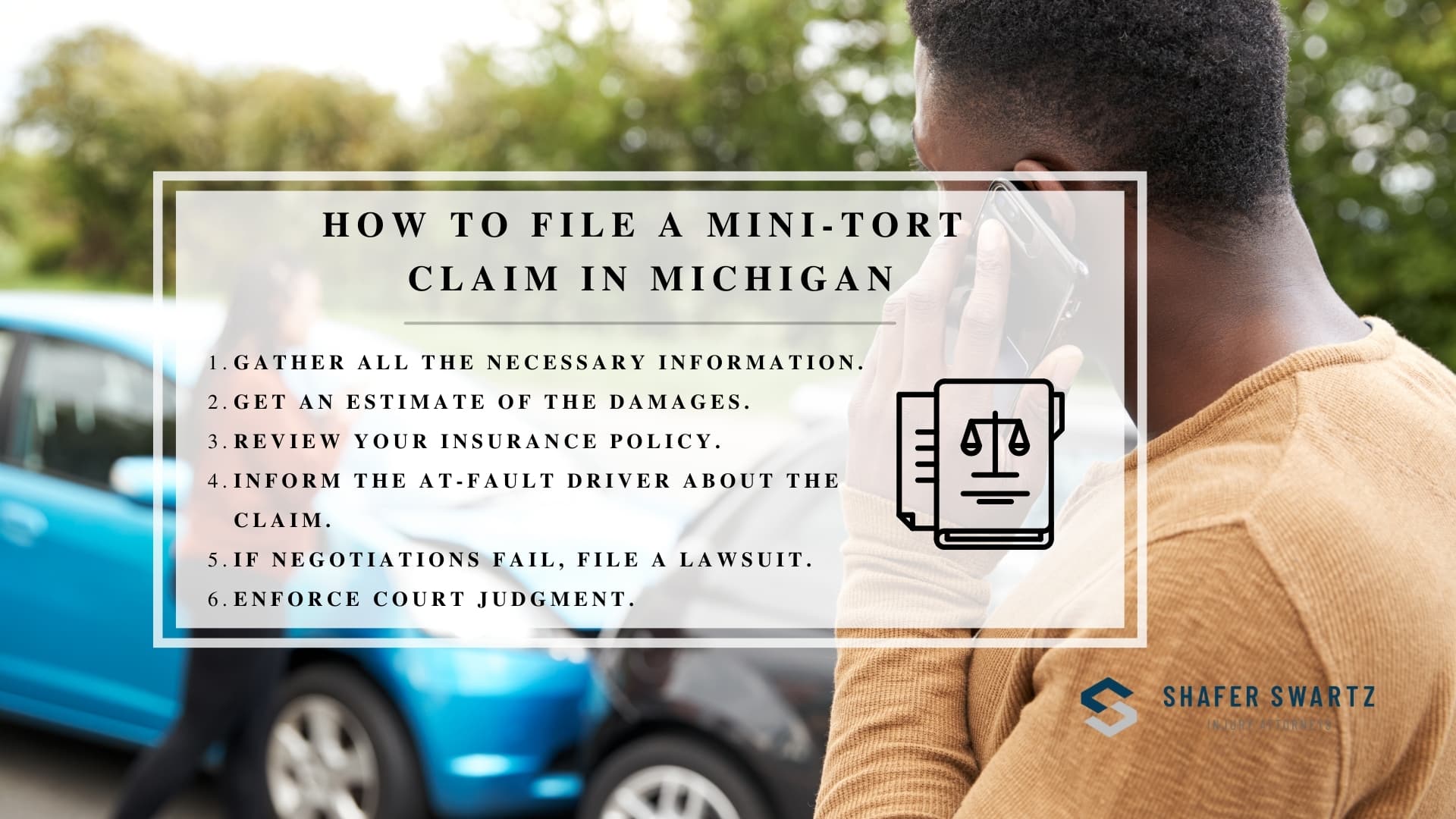

How to File a Mini-Tort Claim In Michigan

In Michigan, you can file a Mini-Tort claim if your vehicle has been damaged in an accident, the other driver was at fault, and your insurance does not fully cover the repair costs. Here’s a step-by-step guide to help you through the process:

-

- Collect all the necessary information related to the accident, including the:

-

- Name & address of the driver

- Vehicle’s model and registration number

- Driver’s insurance agency and policy number

- Driver’s license

- Police report

- Photographs of the accident scene and the damages to your vehicle

- Witness statements

-

- Get an estimate of the damages to your vehicle from an authorized repair shop. Make sure to obtain a written estimate that includes all the necessary repairs and costs.

- Review your insurance policy to ensure you’re eligible to file a Mini-Tort claim. In some cases, your insurance policy might cover the entire repair costs even if the other driver is at fault, especially if you have broad collision coverage.

- If you don’t have collision coverage or your insurance does not cover the entire costs of repairs for your damaged vehicle, inform the at-fault driver about your intention to file a Mini-Tort claim. Provide them with the repair estimate and request payment for the damages. Keep records of all communication.

- If the at-fault driver has limited property damage liability coverage, the insurance company will pay your claim after evaluating the provided documents. If they refuse or offer an insufficient amount, you may consider negotiating further. The at-fault driver can also agree to pay for the damages without involving insurance companies.

- If negotiations fail, you can file a lawsuit in a small claims court against the at-fault driver. Small claims court is designed to handle disputes involving smaller amounts of money without the need for expensive legal representation. You will need to file the necessary paperwork, pay a filing fee, and attend the court hearing.

- If the court rules in your favor, you will receive a judgment. If the at-fault driver still does not pay voluntarily, you might have to take additional legal steps, such as garnishing their wages or seizing their assets.

- Collect all the necessary information related to the accident, including the:

Michigan Mini-Tort Law Updates

For accidents occurring after July 1, 2020, the recovery limit for Mini-Tort claims has increased from $1,000 to $3,000. This means that individuals involved in minor car accidents in Michigan can now recover up to $3,000 from the at-fault driver to cover vehicle damage costs not covered by their own insurance.

How Long Does a Mini Tort Claim Take

In Michigan, the statute of limitations for a Mini-Tort claim is generally three years from the accident date. If you don’t file the claim within this time frame, you may lose the opportunity to recover damages for your vehicle.

Furthermore, the duration of Mini-Tort claims in Michigan can vary widely based on several factors, and the exact timeline can be different for each case. Here are some factors that can influence how long it takes to resolve a Mini-Tort claim:

-

- Disputes and Complexity. If there are disputes about liability, the extent of damages, or other complexities, the resolution process can be prolonged.

- Claim Response. If the at-fault driver and the insurance company promptly assess the claim and agree to pay, the process can move faster.

- Legal Proceedings. If you need to file a lawsuit, the legal process, from filing to the court date and judgment, can take several months.

Who Pays a Mini Tort Claim

When you file a Mini-Tort claim, the responsibility to pay for the vehicle damages will either fall on the at-fault driver or their insurance company. If the driver who caused the accident has limited property damage liability insurance, their insurance company will cover your vehicle damages, but only up to the $3,000 limit. However, if the at-fault driver doesn’t have this specific insurance coverage, it becomes their personal responsibility to pay for the damages, with the same maximum limit of $3,000. So, when pursuing a Mini-Tort claim, you need to determine whether the at-fault driver’s insurance can cover your damages or if you’ll need to seek payment directly from the driver if their insurance doesn’t suffice.

How Do Deductibles Affect a Mini Tort Claim

Collision coverage in auto insurance plans commonly includes a deductible. A deductible is the amount of money you agree to pay out of your own pocket before your insurance coverage kicks in to cover the remaining costs of repairing your vehicle. Generally, if you opt for a higher deductible, your monthly or annual insurance premiums will be lower.

Deductibles can affect Mini-Tort claims indirectly. If you have limited or standard collision insurance, you are obligated to pay the deductible amount you have chosen upfront, even if you are not at fault in the accident. After paying your deductible and getting your car repaired, you can file a Mini-Tort claim against the at-fault driver, allowing you to recover both the deductible and any additional costs beyond your insurance coverage.

However, it’s important to note that Michigan’s Mini-Tort limit stands at $3,000. Any expenses exceeding this cap become your responsibility. Hence, it’s best not to carry a deductible of more than $3,000, especially if you have limited or standard collision coverage. By keeping your deductible within this limit, you ensure that you won’t face unexpected out-of-pocket expenses.

Legal Experts That Can Assist Your Mini-Tort Claim

Repairs caused by car accidents can be frustrating and costly. Learn how to get compensated for car damage if you are not at fault. Consult our team of experienced Michigan car accident lawyers to get an expert’s opinion on mini-tort claims. At Shafer Swartz PLC, we can help you navigate complicated state auto insurance laws and simplify things for you. Call us today at (231) 722-2444 or contact us here to schedule an appointment.